Analysis Report of China Tourism Market in the First Half of 2023

Image source @ vision china

Wen | maidian

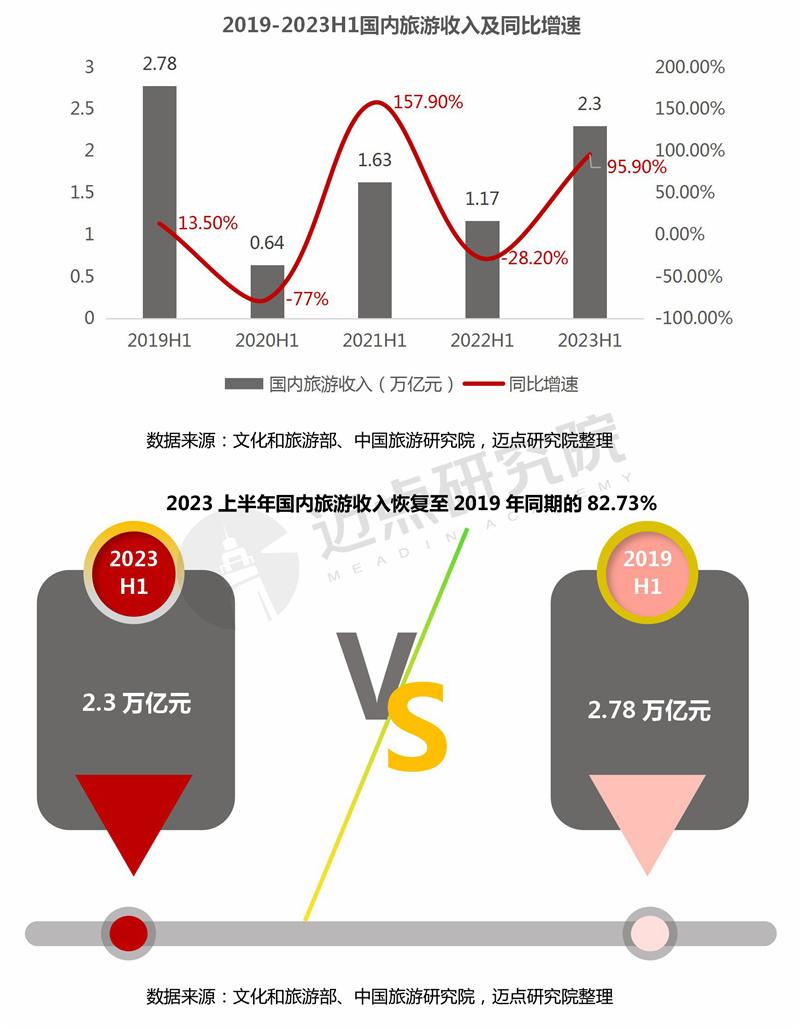

Since the beginning of 2023, influenced by multiple factors such as favorable macro policies and good economic development, the tourism market has been resilient and growing continuously during the Spring Festival, Qingming Festival, May Day and Dragon Boat Festival holidays, and the "Mid-term Examination" report card is eye-catching. According to the data of domestic tourism in the first half of 2023 released by the Ministry of Culture and Tourism, in the first half of the year, the total number of domestic tourists was 2.384 billion, an increase of 929 million over the same period of the previous year and a year-on-year increase of 63.9%; Domestic tourism revenue (total tourism expenditure) was 2.3 trillion yuan, an increase of 1.12 trillion yuan or 95.9% over the previous year. It can be seen that the number of domestic tourists and income increased significantly in the first half of the year, and the tourism industry entered a new channel of comprehensive recovery.

1. Domestic tourism data in the first half of the year: the number of visitors and tourism revenue "double growth" year-on-year, but there is still a certain gap with the same period in 2019.

Domestic tourist arrivals: According to the data released by the Ministry of Culture and Tourism, in the first half of 2023, the total number of domestic tourists was 2.384 billion, an increase of 929 million over the same period of the previous year and a year-on-year increase of 63.9%. Among them, the number of domestic tourists of urban residents was 1.859 billion, a year-on-year increase of 70.4%; The number of domestic tourists of rural residents was 525 million, a year-on-year increase of 44.2%. Quarterly: In the first quarter of 2023, the total number of domestic tourists was 1.216 billion, a year-on-year increase of 46.5%. In the second quarter of 2023, the total number of domestic tourists was 1.168 billion, an increase of 86.9%.

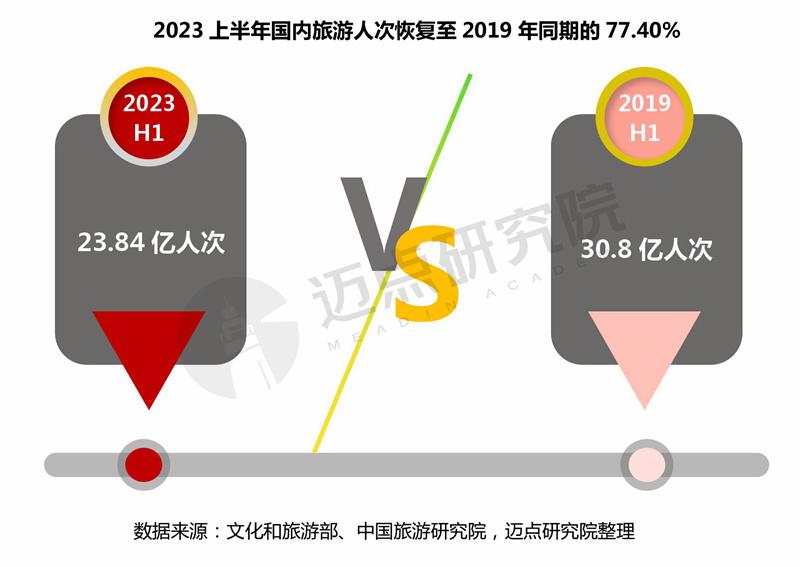

Comparing the number of tourists in each quarter from 2020-2023Q2, the number of tourists in 2023Q1 and 2023Q2 reached a new high in four years, and the number of tourists recovered obviously in the first half of 2023. Further comparison with the tourism situation in the first half of 2019: the number of domestic tourists in the first half of 2019 was 3.08 billion. By comparison, there is still a certain gap between the number of domestic tourists in the first half of 2023 and the same period in 2019, and it has returned to 77.40% of the same period in 2019.

Domestic tourism revenue: In the first half of 2023, domestic tourism revenue (total tourism expenditure) was 2.30 trillion yuan, an increase of 1.12 trillion yuan or 95.9% over the previous year. Among them, urban residents spent 1.98 trillion yuan on travel, a year-on-year increase of 108.9%; Rural residents spent 0.32 trillion yuan on outings, a year-on-year increase of 41.5%.

Comparing the domestic tourism revenue from H1 in 2019 to H1 in 2023: In 2023, the domestic tourism revenue increased significantly, which was the highest since 2020. However, compared with 2019H1, the difference was 0.48 trillion yuan, and it recovered to 82.73% of 2019H1.

2. Inbound and outbound tourism in the first half of the year: the prosperity index of outbound and inbound tourism markets both exceeded the same period in 2019; The per capita consumption of outbound travel increased significantly, and "Hong Kong and Macao" led the recovery process of outbound travel; The number of entry-exit personnel increased by about 170% year-on-year.

According to the data of China Outbound Tourism Market Prosperity Report and China Inbound Tourism Market Prosperity Report released by the World Tourism Alliance in the first half of 2023, the outbound tourism prosperity index in the first half of 2023 was 28, which was 21 higher than that in the same period of 2019, and the outbound tourism was "U-shaped" and gradually recovered, instead of bottoming out quickly; In the first half of 2023, the inbound tourism boom index was 15, which was 13 index points higher than that in the first half of 2019 before the epidemic. However, due to the relatively complicated approval process of international route adjustment, the fragmented service chain of inbound tourism products, the closure of inbound tourism enterprises and the serious brain drain, it is difficult for the inbound tourism market to reach the level of 2019 in the short to medium term, showing a trend of "orderly recovery and fluctuating recovery".

According to the latest data of Alipay’s outbound platform: From January to June 2023, the per capita consumption of Alipay users for outbound travel increased by 24% compared with 2019. In terms of popular destinations, in the first half of 2023, the top ten outbound destinations in terms of transaction volume were: China, Hong Kong, China, Macau, Japan, Thailand, France, South Korea, Australia, Canada, Britain and Xinjiapo. China tourists have once again become an important force driving global tourism and offline consumption. Judging from the number of outbound tourists, the top ten tourist destinations are Shenzhen, Shanghai, Guangzhou, Beijing, Hangzhou, Foshan, Dongguan, Zhuhai, Chengdu and Wuhan. It can be seen that outbound travel is mainly concentrated in first-tier and new first-tier cities, and the five cities of Greater Bay Area, the "Guangzhou-Shenzhen-Foshan-Dongzhu", are also the main force of outbound travel.

Since the beginning of 2023, the National Immigration Bureau has continuously optimized and adjusted the exit and entry management policies: on February 20th, Guangdong-Hong Kong-Macao Greater Bay Area mainland cities implemented the endorsement policy for talents traveling to and from Hong Kong and Macao on a pilot basis, and on May 15th, 2023, it fully resumed the implementation of four measures, including the "National General Office" for mainland residents to travel to Hong Kong and Macao. With the convenient optimization of Hong Kong and Macao tourism policies, many provinces in China have organized a number of Hong Kong and Macao tour groups, and the number of mainland tourists entering Hong Kong and Macao has been rising. According to the data released by the Hong Kong Tourism Board, in the first half of 2023, there were nearly 13 million visitors to Hong Kong, including about 10 million mainland visitors, accounting for about 77%.

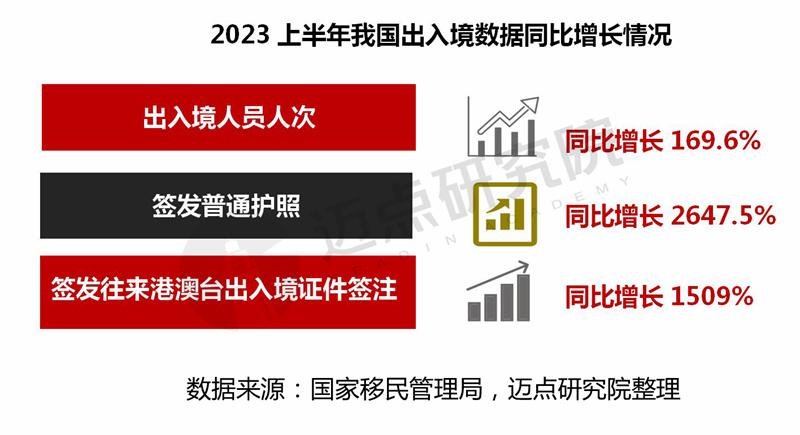

In addition, according to the latest data released by the National Immigration Bureau: in the first half of 2023, a total of 168 million entry-exit personnel were inspected, an increase of 169.6% year-on-year; More than 10 million ordinary passports were issued, a year-on-year increase of 2647.5%; 42.798 million endorsements of entry and exit documents for Hong Kong, Macao and Taiwan were issued, up by 1509% year-on-year, which further reflected the strong recovery of China’s entry and exit tourism.

1. Tourism data of some provinces in the first half of the year

According to the incomplete statistics of Maidian Research Institute, as of July 24th, nine provinces (municipalities directly under the Central Government and autonomous regions) have published the tourism data of the first half of the year. Compared with the same period in 2022, due to the low base in 2022, the number of tourists and tourism revenue in all provinces and regions showed positive growth, and the overall recovery was obvious.

Compared with other provinces, Yunnan Province ranks first among nine provinces and cities in terms of tourism reception and tourism revenue, with 539 million tourists received and total tourism revenue of 693.4 billion yuan, both exceeding the same period in 2019. In 2023, Yunnan Province launched "There is a Life Called Yunnan", and in just four months, the whole network read more than 9 billion people, which continued to ferment and extend, such as cooperating with China Tourism News to column "There is a Life Called Yunnan" and planning to publish 10 boutique tourist routes of "There is a Life Called Yunnan, Traveling to Yunnan in a Cool Summer". Behind this phenomenon, on the one hand, it reflects the strong recovery of the tourism market in Yunnan Province, on the other hand, it also represents the future shift of the tourism model-paying more attention to life and experiencing holidays in depth.

In the first half of 2023, the cultural tourism market in Jiangsu Province was "bright", receiving 478 million domestic and foreign tourists, up 98.3% year-on-year, achieving a total tourism revenue of 610 billion yuan, up 83.5% year-on-year, and its recovery was better than that of the whole country. In addition, according to the business data of UnionPay, the total consumption of cultural tourism in Jiangsu Province in the first half of the year was 252.359 billion yuan, up 31.8% year-on-year, accounting for 10.2% of the country, ranking first in the country. The achievement of these achievements is closely related to the series of supporting policies of the Provincial Department of Culture and Tourism, such as the introduction of the "15 Articles of Suzhou Culture and Tourism" policy, the arrangement of special funds of 90 million yuan to support 130 projects, and the award of 26 million yuan to travel agencies and grade travel homestays, so as to fully promote the comprehensive recovery of the cultural and tourism market in the province.

2. Tourism data of some cities in the first half of the year

At the city level, according to incomplete statistics, six cities released tourism data in the first half of the year: the number of tourists and income of each city showed "double growth", with the growth of key tourist cities such as Zhangjiajie and Sanya being the most obvious. Taking Zhangjiajie as an example, in the first half of 2023, the city received a total of 18.8922 million domestic and foreign tourists, an increase of 185.40% year-on-year; Tourism revenue reached 25.268 billion yuan, up 162.86% year-on-year. It can be seen that the number of tourists and tourism revenue both increased by over 100% year-on-year. As early as the end of 2022, Zhangjiajie declared "2023 as the year of comprehensive tourism recovery in the city", held the cultural tourism consumption season in May, issued the "Implementation Plan of Zhangjiajie Tourism Marketing Award in 2023" in June, and will hold the first China (Zhangjiajie) conference series in September, so as to comprehensively promote the city’s tourism recovery through "consumption season, conference and marketing award" and other measures.

1. Performance of tourism data of each holiday

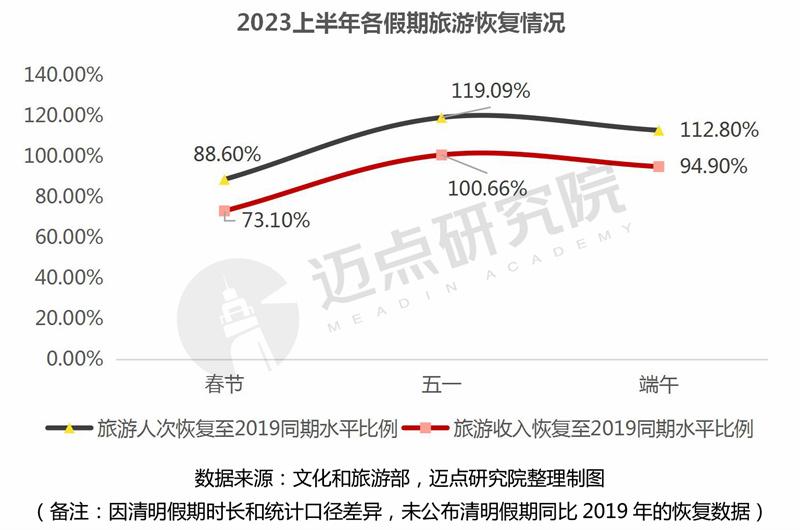

According to the data of the Ministry of Culture and Tourism, during the four holidays of Spring Festival, Qingming, May Day and Dragon Boat Festival in the first half of this year, the number of domestic tourists increased by 23.1%, 22.7%, 70.8% and 32.3% respectively, and the domestic tourism revenue increased strongly by 30.0%, 29.1%, 128.9% and 44.5% respectively. The resilience and continuous growth of the tourism market have dominated the basic pattern of comprehensive recovery of the domestic tourism market.

Further from the comparison between the holidays and the same period in 2019, according to the comparable caliber, during the Spring Festival, May Day and Dragon Boat Festival, the number of domestic tourists recovered to 88.6%, 119.09% and 112.80% of the same period in 2019 respectively, and the domestic tourism income recovered to 73.1%, 100.66% and 94.90% of the same period in 2019 respectively. It can be seen that the May Day holiday is a turning point (the number of trips and tourism income both exceed the pre-epidemic level), which indicates that the domestic tourism market has fully recovered and turned into normal development. From the analysis of the May Day holiday data in various provinces and cities, the trend of "recovery and turning point" is further reflected. For example, the number of tourists and income in nine provinces and regions such as Yunnan, Shandong, Liaoning, Heilongjiang, Tianjin, Inner Mongolia and Jilin have all recovered or exceeded the level of the May Day holiday in 2019, and the per capita tourism expenditure in Beijing, Hainan, Shanghai, Zhejiang and Hunan has exceeded 1,000 yuan.

2. The characteristics of the holiday tourism market

During the Spring Festival holiday, the long-distance tourism market led the recovery, and "annual taste tour", ice and snow tour and quality holiday were sought after. According to Ctrip data, cross-border air ticket orders for the Spring Festival in 2023 increased by more than 4 times; According to the data of Qunar platform, the average radius of tourists’ travel during the Spring Festival increased by over 50% compared with 2022, and the travel distance of each passenger increased by an average of 400 kilometers compared with last year. At the same time, influenced by China’s traditional Chinese New Year customs, seasons and other factors, visiting temple fairs, experiencing ice and snow sports, punching in cultural exhibitions, and participating in non-legacy folk activities are still hot topics for Spring Festival travel.

During the Qingming holiday, the local outing and "one-day spring outing" are hot. Qingming holiday in 2023 is a one-day holiday, so local and close-up "one-day spring outing" has become the choice of most people. According to the data of Ctrip. com, the booking volume of one-day tour products in Qingming holiday has increased by more than 5 times compared with the same period of last year, and short-distance travel is hot, and the order for self-driving car rental has increased by more than 10 times year-on-year. In addition, the Qingming holiday coincides with the "spring blossoms" season all over the country, and outdoor activities such as hiking, mountaineering, flower viewing and camping are also popular.

During the May Day holiday, the scene of "people following the crowd" reappeared in scenic spots, and the popularity of cross-city and inter-provincial tourism increased significantly. The popularity of traditional popular tourist destinations did not decrease, and the emerging online celebrity cities "broke the circle", and parent-child play, non-legacy, leisure vacation and rural tourism were favored. During the "May 1" period, the country welcomed the "blowout" travel of tourists, and the passenger flow in many places broke through the historical record one after another. The scene of "people following the crowd" in popular attractions such as Hangzhou West Lake, Nanjing Confucius Temple and Beijing Summer Palace reappeared. According to Ctrip’s "May 1 Travel Data Report in 2023", the flight distance of users during the "May 1" holiday reached a four-year peak, the travel radius increased by 25% compared with the same period of last year, and inter-provincial hotel bookings accounted for over 70%. From the destination point of view, Beijing, Hangzhou, Dali, Xiamen and other places are still hot, and online celebrity cities such as Chongqing, Changsha and Zibo, and minority destinations such as Changxing and Xianju have attracted much attention.

During the Dragon Boat Festival holiday, domestic tourism demand continues to recover, inbound and outbound tours meet a small climax, people return to life, and theme tours such as folk experience tours, leisure tours that pursue a sense of relaxation, cultural tours of music festivals and art exhibitions and performing theatres, and citywalk are favored. According to the data of the Dragon Boat Festival travel report released by Ctrip, Qunar, Feizhu, Mama Donkey and Tongcheng, the Dragon Boat Festival holiday is mainly short and medium-distance, and the booking of Zhou Bianyou with short trip and convenient transportation is hot. At the same time, the inbound and outbound tourism market ushered in a small climax during the Dragon Boat Festival holiday. According to the data of the National Immigration Bureau, the number of people entering and leaving the country recovered to more than 60% in 2019. From the perspective of product selection, unlike the "special forces" punch-in tour on May 1, tourists return to life during the Dragon Boat Festival holiday, and the "relaxation" tour is hot. At the same time, the traditional culture represented by dragon boat races, dumplings, and garden parties, and the trend culture represented by music festivals and art exhibitions have their own magical powers, bringing rich tourism consumption choices to domestic tourists.

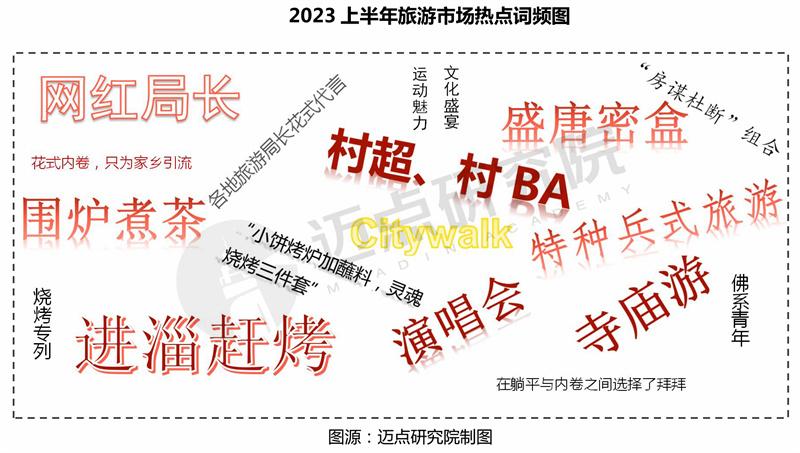

2023 is a year of vigorous and comprehensive recovery of the tourism industry. Tourism practitioners are trying to find a breakthrough through various efforts, "both adapting and changing", so hot spots in the tourism market frequently occur in the first half of 2023. It is beneficial and enlightening for government departments, industry managers, enterprise market players and service practitioners to gain insight into the new trend of tourism industry, explore the new fashion of tourism consumption, and study new ways of playing tourism through new tourism words and phenomena.

Hot spot 1: "Director online celebrity" —— Fancy endorsement by the directors of local cultural tourism bureaus, and new exploration of tourism marketing.

Hot spot 2: "Cooking tea around the stove"-ceremonial consumption, tourism atmosphere economy, new formats driving new consumption

Hot spot 3: "Secret Box in the Prosperous Tang Dynasty"-IP cultivation of cultural tourism, deep experience and interaction of tourism, and promotion of national marketing.

Hot spot 4: "Go into Zi to catch the roast"-gourmet tour, and mass consumption is still an important force driving the recovery of the consumer market.

Hot spot 5: "Temple tourism"-escape from pressure and spiritual sustenance, and the demand for spiritual meditation and healing tourism products is strong.

Hot spot 6: "Village Super and Village BA"-National Movement, Integration of Sports and Tourism to Promote the Development of Rural Tourism Economy

Hotspot 7: "Special Forces Travel" VS "City Walk"-High-intensity and fast-paced special forces travel vs urban deep immersion experience tour, after retaliatory and compensatory tourism, the change from quantity to quality.

Hot spot 8: "Concert Economy"-The integration of "performing arts and tourism" will stimulate the economic growth of urban tourism industry chain.

Taking stock of the hot topics and phenomena in the tourism market in the first half of 2023, we can find that with the normalization of travel, the recovery of the cultural tourism market is fierce, and the phenomenon of "special forces" retaliatory and compensatory tourism consumption is frequent; After the opening up, the competition in the tourism market has become more intense, which is evidenced by the fact that the directors of local cultural tourism bureaus have endorsed local tourism and robbed market traffic. Diversified tourism consumption demands, such as "cooking tea around the stove", "interactive experience tour in the prosperous Tang Dynasty", "spiritual healing tour in the temple", "special forces", "Citywalk" immersed city tour, "going to a city for a concert" and so on, have inspired local governments and tourism market entities to constantly innovate the supply of products and services. The recovery of tourism consumption market is gradual, with high-frequency and low-price mass tourism consumption taking the lead, while the recovery of low-frequency and high-price long-distance travel and outbound travel is relatively slow; The phenomenon of stratification of tourism consumption is more prominent, and "consumption degradation" and "consumption upgrading" coexist at the same time. Some people seek "special forces tour" with high cost performance, while others pay for "a sky-high concert ticket".

In the first half of 2023, the overall tourism market showed a trend of high opening and steady walking: the number of domestic tourists was 94.23% of the whole year of 2022 (2.53 billion); Domestic tourism revenue (total tourism expenditure) is 2.30 trillion yuan, 0.26 trillion yuan higher than the whole year of 2022 (2.04 trillion yuan), that is, "it takes half a year to complete the performance of the whole year of 2022". In addition, according to the semi-annual performance pre-announcement of tourism listed companies, according to statistics, nearly 40% of enterprises have recovered or even exceeded the profit level before 2020. It can be seen that the recovery of domestic tourism market has been established, but the recovery of inbound and outbound tourism is slow due to many factors such as routes, visas and family financial situation.

Looking forward to the second half of the year, we will usher in the traditional tourist season-summer vacation and the Mid-Autumn Festival and Eleventh Holidays. At present, the summer tourism season is coming. From the demand side, there is a strong demand for theme tours such as parent-child tours, study tours and summer vacations. According to the summer travel order data released by OTA platforms such as Ctrip and Tuniu, by the middle and late June, summer parent-child travel orders accounted for more than 30% of summer orders, up more than 7 times year-on-year, basically returning to the pre-epidemic level; The booking volume of research products has exceeded the same period in 2019; The search heat of summer country tour is more than 20% in the same period of 2019. In terms of outbound travel, the popularity of summer travel bookings in Hong Kong and Macao has soared, and Europe has become the main destination for summer outbound travel. Switzerland, Italy, Greece, Spain, Portugal and other products are highly popular. From the perspective of the supply side, the cultural travel merchants are "gearing up", actively adapting to the consumption trend, promoting the iteration of traditional formats, timely launching explosive new products and new formats that meet the expectations of mass summer consumption, and continuously expanding effective supply. Tourist destinations have launched fancy activities such as music festivals, beer festivals and concerts in order to attract more young customers in the summer. On the policy side, in view of the difficulty in booking tourist attractions, the General Office of the Ministry of Culture and Tourism issued the Notice on Further Improving the Open Management Level of Summer Tourist Attractions to make arrangements for booking management, flexible supply, product innovation and market order, so as to better meet the tourism needs of the broad masses of the people. At the same time, local governments have intensively introduced measures such as issuing tourist vouchers and preferential tickets for scenic spots to further explore the local summer tourism market and actively guide tourism consumption.

The "booming supply and demand" of the summer tourism market, policy blessing and consumption promotion are expected to reach the peak of domestic travel throughout the year, and will also lay an excellent foundation for the comprehensive recovery of the domestic tourism market in the second half of the year. Comparing the tourism data in the first half of 2023 with the domestic tourism data in the whole year of 2019-the number of tourists reached 6.006 billion and the total tourism revenue was 6.63 trillion yuan. To reach the level of 2019, there is still "catching up space" of "3.676 billion passengers and 4.33 trillion yuan" in the second half of the year. The pressure is self-evident, and the challenge is still severe. Whether we can create another miracle will not only test the development resilience and vitality of the "invisible hand", but also test the wisdom and ability of the "visible hand".